I remember when they installed one out in Littleton (suburban Denver) - it flows traffic spectacularly but it took years, maybe even a decade for people to get used to it.

I once came upon it and found a full size four door sedan in the (raised) island in the middle with four befuddled teenagers standing around shaking their heads. They had plowed into the traffic circle straight ahead, jumped the raised embankment and landed right in the center island.

But the roundabout saved them. If they were not paying attention, as clearly they weren't, then they could have had a collision in the centre of an intersection. Better to end up in the he Center than t-boning a car.

As a Coloradan, this is something that we have been especially hard hit by. More and more people are living in/around our national forests in the mountains. Naturally, they don't want to deal with fires, nor the remnants left behind (charred landscape for a decade or more.)

But as this article alludes to, it has to burn. It does naturally. We have to let go - we are wasting valuable resources to fight these fires. People have _died_ fighting these fires. And for what? So your house doesn't burn down?

I'm sorry, but a fire is typically a slow-moving natural disaster. It rarely strikes without a fair warning. I've been saying for years now that if you live in a potential burn area, know where your irreplaceables are, carry fire insurance, evacuate and LET IT BURN.

"Carry Fire Insurance" -- That raises the fundamental economic issue, which surprisingly the Economist was silent; a policy of fire suppression is a subsidy for the people who choose to live int he forest. If there wasn't a policy of fire suppression, a home owner wouldn't be able to get fire insurance, and without it, they wouldn't be able to get a mortgage so fewer homes would be built in the forest.

Houses can also be made much more fire resistant than they are. Use metal and masonry for the exterior surfaces rather than wood and asphalt, for example. Keep the fuel and vegetation away from the walls. Build a masonry fence as a fire break. It's all just common sense.

Some friends of mine built a house this way in Montana, and the firefighters told them that if all Montanans built their wilderness homes that way, their job would be a lot easier.

You can find a lot of information on this by googling for "fire resistant home".

Fires will jump over that masonry. Unless you live in a concrete dome, the fire will get across. These are infernos not unlike the fires of hell. Fire is almost raining down on you. Fire resistant doesn't work in the middle of a serious wildfire.

Societies subsidize people who live in flood plains because of agriculture, infrastructure and logistics. Essentially, we get far more OUT of people living in MOST flood plains than we put in with respect to subsidies.

Consider MOST of the coastal cities. We, obviously, get WAY more OUT of Houston, Galveston and New Orleans, for example, than we put in. Those three ports are enormously important to us. If they disappeared tomorrow, you would discover why they were important the hard way.

Similarly for people living in midwestern flood plains. We will typically get far more out of them than we put in. Try feeding the world, with currently known agricultural technology, while not using any land in flood plains and you'll see what I mean. Even if you could somehow manage to do it... and I don't think you could.... but even if you could, you would cause enormous damage to the ecological tapestry of the continent. You would have to move MATERIAL amounts of water and soil at a minimum. It's best to subsidize the farmers to do what they do and make sure they're not disturbed in their endeavors. And, yes, many of those farmers and agribusinesses will be in flood plains.

Now I'm not saying ALL flood plains in the midwest or on the coast are critical infrastructure. New York, Houston and New Orleans are far more critical to our survival than... say... Miami, Myrtle Beach or Malibu. So obviously, I'm not saying that ALL port cities or ALL midwestern flood plains are critical. But there are definitely some places in this nation that merit sizable subsidies to keep people living and working there. It's the nature of the beast when you're talking about engineering an empire.

For any activities that really are that valuable, there is no need for a subsidy. The revenue from the activity in those cases exceeds the costs of dealing with the disaster.

The efficient thing to do is end the subsidy, and have all the less valuable activities whose benefits don't exceed the costs relocate or cease.

A scholarship is an educational subsidy. Should we issue a moratorium on scholarships? Should we discontinue subsidies for solar energy companies? How about the billions in R&D tax subsidies that we give to pharmaceutical/industrial/healthcare companies each year to develop new drugs, treatments, and machinery?

The market doesn't always know what is right. To be more specific: the market is short-sighted and greedy, and can self-destruct an economy if left unregulated. We need to subsidize activities that have large costs in the short term, but return more over the long run to society. Or else they won't happen.

State funded 'generic' scholarships simply rise the cost of tuition. Good state schools are a much better use of funds as they drive down for profit education costs to be cost competitive. Schools can easily offer scholarships at minimal costs as a form of price discrimination, but public scholarships tend to simply result in administrative bloat.

Should we discontinue subsidies for solar energy companies?

How about the billions in R&D tax subsidies that we give to pharmaceutical/industrial/healthcare companies each year to develop new drugs, treatments, and machinery?

These should also be stopped, it's fine to fund public R&D but private R&D has terrible ROI. Drug companies spend more on advertising than R&D and really don't need help. For a solid example, the US could have a 10 year strategic food reserve for 1/10th the cost of current agro subsidies that directly result in massive health issues.

PS I agree that markets are often inefficient, but subsidies then to be horrible ways to correct them. Taxes tend to be much more efficient.

Taxes and subsidies are two sides of the same coin.

They are often used in conjunction to achieve specific policy ends. If you are pro taxes, you are pro subsidies. Perhaps not on the specific, case-by-case basis, but overall you are arguing for free market distortion through the yin and yang of government policy.

I won't address your specific points as everyone has different opinions on policy, but no one has the data to rigorously defend their opinions.

I simply want to refute the notion that we can allow free markets to allocate all resources within the economy.

Ok we can side step the specific examples and I agree with your point. But, at the meta level I still think taxes are generally a better solution independent of policy.

Taxes are much more scalable than subsidies. AKA if A is better for society than B but B is cheaper to produce then taxing B can balance things fairly easily with consumers paying society for the external costs. But, subsidizing A is an unbound cost, adds administrative overhead, and promotes consumption of A and or B.

The downsides of Taxes is there often regressive, but for something like alcohol, pollution, or speeding societal costs are often independent from a persons net worth.

Ending federal student loans would do more to reduce higher Ed inflation than anything else. It's unpopular because the people smart enough to understand economics aren't the ones continuing to vote for expanded federal loans.

Taxing CO2! Then how would we breathe! Think of the effect on laborers that breathe more strenuously than the rest of us. They be impoverished! On a serious note, you're implying that CO2 has a deleterious effect. Any scientific studies to back that claim?

If you want more people being educated, you should subsidize education.

If you want more R&D, you should subsidize R&D.

If you want more people living in burn zones, you should subsidize living in burn zones.

I think I join most Americans in saying that I'd rather more people be educated, I'd rather have more R&D, and I wouldn't rather more people live in burn zones.

Efficiency must be balanced, though. Say that we end the subsidy on agricultural flood plains, which drives up the cost to farmers, who become less competitive vs imported food. They decide to close up shop and do something more profitable, since they can't complete with imports. The end result is an increase in efficiency but a loss of food security.

I'm sure other people have thought this through much better than what I just said. But it seems to me to be a reasonable argument.

If your goal is people growing more food relative to baseline, you should subsidize food (which we do, intensively).

If your goal is people living in flood zones, you should subsidize living in flood zones (e.g. by insuring it, which we also do).

We need an answer to the latter question in this case, not the former. And one is readily at hand: the political interest of those who live in flood zones. Maybe there's some other justification, but I'll confess I'm skeptical that this outcome is globally utility maximizing relative to alternative policies.

So a worker that works in Houston ought not have flood protection? Who pays when his house floods? "Industry?" Then prices rise for everyone instead of isolating the risk to those that choose to buy flood insurance.

Most floods are only a few inches deep. It isn't expensive to simply build the house up a foot or two, or bulldoze a mound and put the house on that. It'll greatly reduce the probability and severity of flood damage.

Houston and New York are also designed with an expectation that those cities will flood. Most buildings in Houston, for example, forgo a basement and instead have a collecting vault underneath them that the rain drains into and from (and leaves more slowly and sustainably). There are fields set aside to ensure that there's land that can flood with minimal impact. County flood control districts will buy up property just to let it be undeveloped.

There are ways to mitigate the risks of living in a flood plain while still reaping the benefits.

How are buildings in NYC designed with an expectation that they will flood? I haven't seen much of that, especially pre-Sandy. Post-Sandy there are some buildings with mounting brackets for walls/sandbags if there's another flood but that's not really designed in.

I'd argue that flood insurance isn't necessarily the same thing, at least in some cases. I live in an area with three rivers and lots of creeks and runs that feed those rivers. It isn't always "natural" for the sections of the river, or those creeks to flood. It takes a lot of rain, in some cases "act of God" levels. Flood insurance seems pretty reasonable in those cases, particularly since in many cases, there isn't a ton of flood preventation infrastructure that has been built with tax money.

> It isn't always "natural" for the [...] the river [...] to flood. It takes a lot of rain, in some cases "act of God" levels.

That's a weird definition for "natural" you're using. I think you mean something more like "typical". Unless you're making a theological point, an "act of God" is quite literally as natural (in the sense of un-artificial) as you can get.

But the grandparent's point was economic. Disaster insurance can't work: the whole idea behind insurance is that "bad stuff" happens rarely to some people, so everyone pools money together to pay for the few who actually needed. Disasters happen broadly, and to everyone who needs it in the affected area. A "correct" insurance scheme there would be tantamount to everyone having to just save money on their own, there's no efficiency. And of course in practice the insurance companies cheat and don't save enough, so people don't actually get paid.

While this is true. It does not mean that they are not "normal." They are just so rare as to allow a party to get out of a contract.

As a society, we cannot ignore the cost of the "Act of God" level disasters when summing up the cost of said disaster. If an insurance companies might be able to avoid paying out on a claim doesn't mean property (or lives) did not get lost.

Just wanted to give some color to BMJ's comment for most people who would not be familiar with the legal boilerplate, as his comment was interpreted as theological by some.

In my mind the issue is pretty simple: if you buy a house in a wild-fire prone area, you should expect a wildfire at some point. Whether or not you want to prepare by a) purchasing insurance or b) wild-fire proofing your house is your prerogative. If you're not willing to take/mitigate the risk, then live somewhere else.

True, but not really relevant. I mean, that article literally (!) calls out flood insurance as a situation where such "acts" are subject to the contract.

> And of course in practice the insurance companies cheat and don't save enough, so people don't actually get paid.

Or changing conditions throw off their actuarial tables, making the company insolvent when reality intercedes. Those changes could be as obvious (at this stage) as climate change, or as subtle as a long-standing practice of preventing forest fires, which while seemingly preventing property loss to fire is actually creating an unstable system which has the capability for much larger destruction than the typical fire.

That isn't true. It's a law that insurance companies must have the money to pay claims. That's what reinsurance protects insurance companies against. People don't get paid because they didn't suffer a covered loss. I was a catastrophe insurance adjuster for Farmers insurance during Katrina and Hurricane Ike and the unpaid damages where often for damages not caused by a covered event: for example a destroyed wooden floor with no evidence of roof leakage would often be denied unless they had Flood insurance. We also have massive amounts of attempted fraud. People attempting to claim full value on a roof that was 20 years old. The amount of fraud in the property insurance business amounts to literally billions. Also denied claims are easily challenged with a public adjuster. I had plenty of debates with public adjusters and there were time when I did legitimately underpay a claim. Damage estimating is a very inexact science. There are dozens of variables such as material cost fluctuations, damage area material cost gouging, contractor shortages they lead to out of state contractors coming in charging higher than the prevailing rate for a given piece of work. The meme that insurance companies are evil is simplistic. The amount of regulation in that industry is astounding. I had to get separate licenses in 18 states. A few other states has reciprocity agreements but generally I had to pass exams just to step foot in a state in any official capacity. I am definitely not referring to health companies though.. Can't speak to that, but the property and casualty side of things isn't as terrible as it's anecdotally portrayed. During Ike, I wrote 12 checks per day which meant 16 hours a day on rooftops wading through debris and occasionally coming across human remains. Yet less than 5% of the claims I worked were denied and generally only partially.

Property and casualty insurance spreads out risk over a large group of people during the same time period. P&C insurers have it easy. They can pay out claims from the premiums that come in, and take the leftovers as their profit.

Life insurance spreads out risk over a large span of time for the same person. Life insurers have to be more careful. They have to invest the premiums wisely, so that they will have exactly enough cash on hand to pay out the amount of the policy on the expected date it comes due (along with some profit). If the person dies earlier than expected, they could lose money. If the person dies later, they could get more profit. Furthermore, if the investment market is unexpectedly good or bad, that affects the insurer's ability to pay the benefit. Life insurers can rely on the fact that while all people eventually die, they don't all croak at once. There's actually a predictable rate, so if you get enough people to buy policies, you're never paying out more than you take in.

Disaster insurance is more like life insurance, but even harder to pull off, because all those benefits are probably going to be paid at exactly the same time. So what insurers have to do is take that gigantic, elephant-choking payout and let each underwriter take a little bite of it, until it's all accounted for. They're spreading the risk over multiple people, long periods of time, and multiple investors. And even so, thanks to the fact that it is essentially an enforced savings scheme, a big enough disaster would be a shock to the financial markets.

But there's no way around that. If a storm destroys one of your windows, you're going to be buying a new window, instead of some other thing that you may have wanted more. If it destroys your whole town, a lot of money is going to shift from savings and investments into construction.

There is some advantage to having disaster insurance. First off, ordinary people are absolutely horrible at reasonably judging risks. Second, we are also pretty bad at compartmentalizing our savings and investments. If you have a 100-Year Flood fund, and a Yellowstone Goes Kablooie fund, and a Bad Tornado Season fund, and your grocery budget stands at $20 for this month, would you have the fortitude to eat nothing but beans and rice for four weeks? And third, institutional investors manage money better than a lot of individuals, and can take better advantage of the tax laws. It isn't hard to just dump everything into the Fideliguard Some of Everything Index Fund, but some people still put all their money in an ordinary commercial bank savings account, where the interest doesn't even cover the monthly service fees, but it still gets taxed.

But as you say, a lot of those advantages can disappear to just one bad actor in the insurance company trying to cheat a little for some personal gain. The best thing people can do to manage disasters is to be aware of their own risks, and to plan ahead only for those scenarios that have a reasonable likelihood of occurring.

in most cases we're talking about people who build their houses in category 1 storm surge / 10 year flood zones and then expect a subsidy when inevitably natures does what it does.

It's exactly the same thing. Flood insurance enables people to build houses in places where there are going to be floods, just like fire insurance enables people to build in tinderboxes. Which would be fine if the person who buys the house there carried a financial burden proportional to the risk.

there isn't a ton of flood preventation infrastructure that has been built with tax money.

All flood prevention infrastructure outside of the dirt berm at the local pond was built with tax money. Been to, say, New Orleans recently?

All of the premium non-hurricane, non-forest land, is taken already by rich people. Isn't it subsidising rich people if we allow them to live on the best land, while others contributing to society elsewhere observe no benefit?

The US states least affected by natural disasters are Alaska, Main, Michigan and Vermont; based on your post, I assume they're filled with rich people?

It is interesting that some of the poorest, white-trash areas of the country are the safest. At least in Maine, the only natural disaster I can remember is the ice storm of 98, which, aside from knocking out power for a week, mostly amounted to an extra week of school vacation that winter.

Almost every region comes with its own set of possible natural disasters. Maybe we are better off pooling everything and just have natural disaster insurance that covers fire, flood, tornado, hurricane, earthquake, blizzard, and so on.

Yes, almost every area has it's own disasters to worry about, but it's a mistake to assume that the frequency and average damage for each type of disaster and each area normalizes out to a similar value.

That is obviously true, but that doesn't stop other insurance industries. A healthy 40 year old women and a 70 year old man with heart disease are going to have different prices for a $1m life insurance policy, but both policies will pay out equally regardless of when they die.

I'm not saying home insurance needs to be the same cost for everyone, but the current situation of specialized policies that vary house to house in each region is overly complex. Plus climate change is changing the risk profile for everyone and the results of which are not yet clearly understood by climate scientists let alone random homeowners.

> but the current situation of specialized policies that vary house to house in each region is overly complex

I actually think it's not complex enough. How else do you accurately price natural disasters into existing homes, whose ownership is often measured in decades? I think any area with a chance over a certain percent of a natural disaster that could cause catastrophic loss of property should require insurance, and the insurance cost should be as accurate as possible to the reality of living in that location.

7. allentown pennsylvania* (actually east, not midwest)

6. dayton ohio*

5. bethesda maryland

4. buffalo new york

3. akron ohio*

2. cleveland ohio*

1. syracuse new york

Hmm, maybe you're thinking of the central US? also known as 'tornado alley'?

The definition of various 'areas' of the US are ill defined, but its clear, at least from my experience living in the midwest and having never experienced a single disaster in the 25 years I've been here, that the midwest is definitely the safest from natural disasters.

Are the astericks there meant to denote midwest? Allentown is further east than Syracuse, Buffalo, and Bethesda, so it isn't midwest.

It is also worth noting that almost all of the cities listed are heavily impacted by snow which it doesn't sound like it was factored in to the ranking. Dealing with large snowfalls have a huge costs although it might not be factored in to normal home insurance since there is generally minimal property damage. It might be interesting to see a cost comparison between dealing with large snowfalls and other less frequent but more damaging weather phenomena like hurricanes or tornadoes.

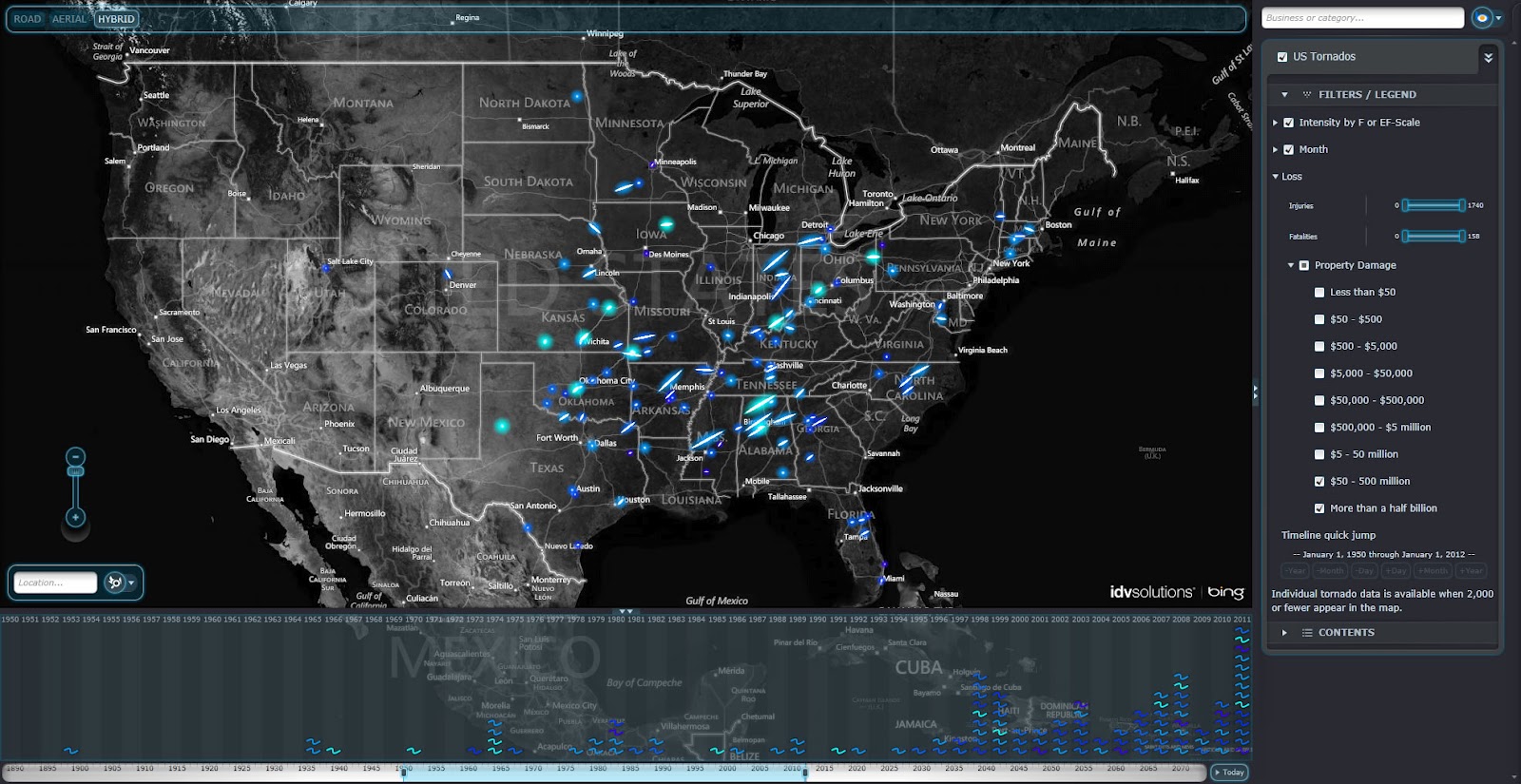

Finally, Ohio certainly sees less tornadoes than most of the midwest, but it still receives a lot compared to the western US. Here is a nice visual summary of recorded tornadoes [1]. This one [2] is of especial interest and shows all tornadoes that have caused $50+ million in damage which would be important when talking about insurance. Tornado alley certainly gets more tornadoes, but Ohio is right up with them in terms of damage mainly due to the comparative development of the various areas.

I think i was thinking of youngstown ohio - i updated the list

As for ohio, I count 6 tornados on there, maybe 7? (i might be reading it wrong)

since 1950?

I'd say thats pretty low risk.

How many earthquakes have we had in that time?

How many hurricanes have caused billions of damage in that time? Floods/draught/etc

> which it doesn't sound like it was factored in to the ranking.

I dont think it was, it was ranked by natural disasters - so unless its a major blizzard it probably wouldnt be measured. (oh they probably didn't include hail either, which is uncommon, but more damaging to property)

I also dont think snow is on the same level as a natural disaster from an insurance risk perspective, but it likely results in greater or at least similar fatalities overall so i think its a fair point.

I'm not arguing the midwest is immune to all danger, i'm only saying living there puts you at lower risk of being affected by a natural disaster - /and/ - that the land there isn't already owned by 'rich people' (to take us back to why i commented in the first place)

Also - i wish that tornado map was interactive, would be great to see more of the filters

Indiana farmland costs $4400/acre to buy, costs $160/acre-year to rent, and produces 150 corn bushels/acre-year or 50 soy bushels/acre-year. That sells for $3.50/corn bushel, and $9.00/soy bushel.

Doing the math, it's pretty easy to guess that all that midwestern land is probably owned by "rich people", too.

I put that in scare quotes because there is some element of circularity involved. If you own 120 acres of cornfields, you have over $500k worth of property. So do you own the land because you're rich, or are you rich because you own the land?

>Doing the math, it's pretty easy to guess that all that midwestern land is probably owned by "rich people", too.

Now do that math with land values in Detroit.

I think its well accepted that land values are generally quite higher on both coasts than the midwest. Agricultural land values are not very useful for estimating the cost of residential land

But there is a lot more agricultural/forestry land out there in America than residential. There are more people living in Cook, DuPage, and Lake counties than the entire rest of the state of Illinois. 53% of the population on 3% the land area.

Ted Turner didn't get to own 2M acres of land by buying in Atlanta. Much of that is bison ranches.

There are a lot of people out there that own no more than 0.25 acre, which is pledged as security for a mortgage.

If you own land outright, free of liens and mortgages, whether rural or urban or in between, you're already way ahead of most people. You may not be actual rich, but "rich" by comparison with your neighbors.

Peering under the covers of agribusiness in the U.S. was somewhat enlightening. It would appear that one should not attempt a farming start-up without at least $1M in the bank, and you will only get about an 8% return on it per year, on average. Small farms simply do not make money; you cannot run a small farm as your sole source of income and expect to earn the equivalent of minimum wage.

So the natural conclusion I reached from my cursory research is that the vast majority of raw acreage in the U.S. is probably owned by investment trusts, who lease it for farming, mining, ranching, and logging, to people who barely earn a profit, and mostly just immediately spend 70% of everything they earn on expenses.

There's a good reason why YCombinator invests in tech start-ups instead of plows and cows.

In the West(-ern US), a great deal of it is actually owned by the federal government[0]. Should it be sold to provide homes for people that otherwise would live in hurricane areas?

I was actually thinking this as well. Higher insurance premiums for homes that are not rated to far exceed what should in practice be possible to experience in a hurricane or fire should be the norm. Actually, my guess is this is coming, as soon as the actuarial tables adjust to the new climate reality (barring political meddling to suppress normal market forces).

As for floods... I dunno, maybe insurance requiring some portion of the house that is higher than the flood plain and that the house is not in danger of becoming unmoored for any sort of sane rates. I imagine that would make housing in places way under the flood plane or that face both floods and hurricanes expensive to build in, which is the point.

"Actuarial tables" are really only used to price life insurance.

Property/Casualty insurance (auto, home, work comp, etc.) are priced by analyzing recent loss experience, then trending loss costs forward (as medical costs & replacement costs go up over time).

Hazards that are infrequent and spatially-correlated (hurricane, tornado/hail, fire) are often priced by using simulations, which take into account the nature of the event, engineering simulations, and insurance policy terms.

Flood insurance is incredibly politicized, as it's handled at the federal level. Floods are typically considered an "uninsurable event" given that if you live in a flood plan, there's a high likelihood that you'll have a loss due to flood--less of an "if" than a "when".

Flood insurance is sold & claims are handled by insurance companies, but it is effectively reinsured 100% by the federal government. Actuarial studies have show the premiums to be highly inadequate, but there has been legislation that aims to reduce that inadequacy.

What I suspected, and what you hint at, is that the insurance market isn't all that efficient in some areas. In some cases because there's limited information, in which case the only way to increase market efficiency is to do more research (which is so open ended it's impossible to know when you're doing "enough"), or to pad the results to account for errors. In other cases it's because there's been too much government interference, or the interference has had unintended side effects (I believe in market interference, I just believe it should almost always be to increase efficiency, where all to often our efforts are to subsidize a segment and that has too many follow-on consequences). Requiring insurance in specific areas might help this.

It does has to burn. This is why we have prescribed burns, to safely burn the forest and reduce future wildfire damages.

The article says that the portion of the budget dedicated to fighting fires keeps increasing, giving less money to land management decided to prevent a lot of the fires we are fighting. Seems to me that continuing on this path will just result in ever increasing costs. We have to let it burn, on our terms.

Logging helps a lot too. I don't get why it's such a controversial topic, I don't advocate chopping down entire forests, but why on earth are commercial loggers not allowed to thin things out?

When have commercial loggers ever "thinned things out?" Since the beginning it's always been a "choose a section of forest and start chopping until nothing is left" industry.

This is patently untrue, at least in the United States. Maybe if you are doing slash-and-burn agriculture in the Brazilian Amazon. Even for clear-cutting, you have to leave a regulated number of stems, of certain diameters, on the piece of land.

Typically, the way you would cut a piece of land is by selectively cutting out the species and grades of lumber that are actually worth money. So one winter you go in and cut the big, high-quality pine, or spruce and fir for saw logs. Another season you might cut out the high-quality veneer-grade hardwood trees. Of course, when you do this, you would also cut a bunch of the junk that is never going to grow into profitable timber, and sell that as pulpwood for making paper, or low-quality logs for making pallets, or sell it as firewood. If you selectively cut like this, it's not particularly difficult to rotate through a series of stands and continue to harvest them indefinitely, and you maintain a variable-age forest that sustains the local wildlife, to boot.

At least on the East coast, it's not really necessary to replant cut sections, even if you do go in and clear cut them, since there is so much residual seed on the ground already, and many of the species will even sprout again from stump. You go through a short cycle of black/raspberries and other scrub growth to fix the soil, then the young softwood/hardwood whips come up through, and within ten years you've got a stand of wood that's ready to be thinned out again, to clean out the junk and let the good wood grow up into profitable timber again.

On the West coast, as I understand it, replanting is more important, since many of the species won't grow from seed UNLESS there has been a forest fire.

The United States is also more forested now than it has been in a hundred years, since so much land formerly cleared for agriculture has grown back as forest. If you could look at Google Earth imagery of New England from 1900 and today, the difference would be astounding.

Clear cutting absolutely did happen in the US. Take a flight over the Pacific Northwest and you can clearly see the effect decades later. Get out into remote areas and you can also see just how stark selective cutting is compared to a pristine landscape.

Second growth is only a step in the ecological process of producing a mature forest. Most of the east coast's regrowth is not representative of the original species, though it is often farther along in the process compared to the west coast. These places take multiple centuries to come back to their former pristine state.

Why does it take so long? Plant species are sensitive to available light and moisture. Canopies regulate this on the ground, but also rely on established plants for their development. Immature, modified or non-existent canopies cannot support the same life.

Selective cutting modifies the canopy. Established growth underneath does not survive, even if it is still alive when the crew goes home. When the canopy recovers in a single century the lower plants can thrive once again.

Well for one, that's not entirely true. Loggers plant just about as many trees as they cut down. Otherwise they'd be out of business pretty quick. And even when they chop, "thinning things out" is a perfectly valid way of logging and is practiced in many places.

Secondly, the question was "why don't they thin things out". Not "why don't we let them thin things out". Implying a change to normal behavior.

Just to play devil's advocate. What about the amount of greenhouse gases released by the fires? We're clearly not succeeding in reducing our greenhouse gases, so why not reduce it where we can?

Compared to the CO2 that has been "permanently" sequestered in the Earth's crust through coal and oil, the trees involved in the fires contain a relatively trivial amount of CO2.

In the US, we are succeeding in reducing the rate of growth in CO2 emission. We're not yet succeeding in reducing total gases. We'd be a lot more successful if we stopped subsidizing the production and consumption of oil and coal. In 2013, the IEA estimates US$548 billion (annually) of global subsidy to fossil fuel. And the IMF calculates that including external costs (pollution), US$5.3 trillion of subsidy in 2015.

You mean the greenhouse gasses that were originally sequestered by the forest into a cellulose matrix and which were inevitably going to be re-released when the tree died and the wood rotted? Yeah, I don't think the process works the way you think it does.

Most of the time when wood rots, it still sequesters CO2. If it didn't, you wouldn't be able to create soil through the accumulation of biomass. All the dirt would be mineral only, and no black soil would exist anywhere. The blackness of black soil is due primarily to carbon. Which isn't floating around in the air.

Seems like the difference in timescale between soil creation and wood decomposition would argue against sequestration occurring "most of the time." Soil biomass might represent only 1% or so of decomposition products. But I haven't seen any actual figures...

Trees are big and take up a lot of room, but there's way way way more dirt than trees. Good soil is actually upwards of 5% organic matter which is non-trivial. 5% of all the good dirt left in the world is a very big number and probably dominates the weight of trees on the planet.

Forest fires are a cyclic phenomenon complemented by forest growth. Best to let nature find its own equilibria and change human processes to be sustainable.

Interestingly, far more wood smoke is released into the air during winter than during peak fire season. If the stated aim is to reduce greenhouse gas emissions then from a cost/benefit perspective moving away from burning wood for heat to a cleaner form of energy makes far more sense than fighting fires.

Recent research has been showing that native americans shaped their forests with fire. It's entirely possible that many of the north american forests intentional human caused fires as part of their normal cycle.

This varies greatly by region, land use, and weather patterns. In some places and years, humans dominate; others, lightning. Because humans tend to start more fires near cities, campgrounds, and other accessible areas, those fires tend to be contained or extinguished quickly. Lightning starts tend to be on ridgelines, near peaks, and in other remote areas that are difficult to reach. Many of the big, long-burning fires are lightning starts, but they also tend to threaten fewer structures. Obviously there are exceptions all around.

I think that's a combination of high winds and young growth. If it is young growth, it's actually illustrating what the article is describing, the young growth trees are young, but not at young s they should be, and they bridge the gap between the undergrowth and canopy. Once the canopy catches in a dense forest, there's a real problem, but a dense forest with undergrowth only on file may be a mild, slow moving (since the wind may be mostly blocked) fire.

>I've been saying for years now that if you live in a potential burn area, know where your irreplaceables are, carry fire insurance, evacuate and LET IT BURN.

If people did that, you couldn't buy fire insurance any more.

Let's look more positively at the problem. Use robots to fight fires. Use robots to manage fuel stocks. Learn more about firefighting as a species. I think we can get a lot better at fighting fires than we are right now.

Is it possible to clear enough brush/trees from around your house that the chance of it catching on fire is small? I've always wondered this, but I've never seen this issue addressed anywhere. Thanks.

EDIT: of course, if your house was left standing in the middle of a fire wasteland, you might want to live there anymore.

Yes, it is possible to make fire-breaks where the fire can be handled.

They have to be very large (and therefore expensive. Both in terms of land and in terms of maintenance) to protect your house against a mega fire though.

Of course, they could be created in preventative fashion to limit the fires so that the size of the forest fires is limited.

While it would have to be "large" for a "mega fire," there are a lot of small and inexpensive things you can do to help protect your home. Things like removing any shurbs around your house are very useful. Won't necessarily save your house, but it's a good start.

Yes it is, and it's actually pretty easy. There are many ways to reduce the chance of a fire hitting your actual living structure and out west there actually are landscaping firms that specialize in doing that. Unfortunately many older homes/properties aren't set up for this so that's when it can get expensive.

Source: I'm a wildland fire fighter. Have seen awesome and terrible uses of fireproofing property.

{kind=link}

I once came upon it and found a full size four door sedan in the (raised) island in the middle with four befuddled teenagers standing around shaking their heads. They had plowed into the traffic circle straight ahead, jumped the raised embankment and landed right in the center island.